🌍 Frontier Markets News, May 15th 2026

A weekly review of key news from global growth markets

Africa

Algeria looks to expand energy influence

Algeria is continuing to expand its energy footprint across Africa, this week sending a delegation from state-owned gas and electricity utility Sonelgaz to prepare for construction of a 40-megawatt power plant in Chad. The project is similar to one under construction in Niger that is due to be completed soon.

Also this week, Algeria signed a crude oil supply agreement with Egypt aimed at strengthening regional energy integration and diversifying Egypt’s energy sources.

Algeria’s state-owned oil company Sonatrach last week signed a $1 billion contract to develop the second phase of the country’s Hassi Bir Rekaiz oilfield, adding roughly 31,500 barrels per day of processing capacity. Algeria, which also last month opened seven exploration blocks to international companies, plans to invest $50-60 billion to double gas production to 200 billion cubic meters by 2030.

Côte d’Ivoire cocoa exports falter

Côte d’Ivoire’s Coffee and Cocoa Council (CCC) this week moved to defuse tensions with farmers who blocked roads demanding payment for unsold cocoa, deepening a crisis in the world’s largest producer of the commodity, CNBC reports.

Cocoa accounts for about 14% of Côte d’Ivoire’s GDP and supports some five million people, but a sharp fall in global prices late last year left many farmers unable to sell their harvest. The government launched a buyback program in January, though many growers say they still have not been paid for beans harvested between October and March.

The sector also faces a looming regulatory challenge as the EU’s anti-deforestation regulation, which takes effect in December, requires importers to prove commodities were not grown on deforested land. An analysis published this week by non-profit Trase found less than half of Ivorian cocoa exports can be traced back to the cooperatives that grew them.

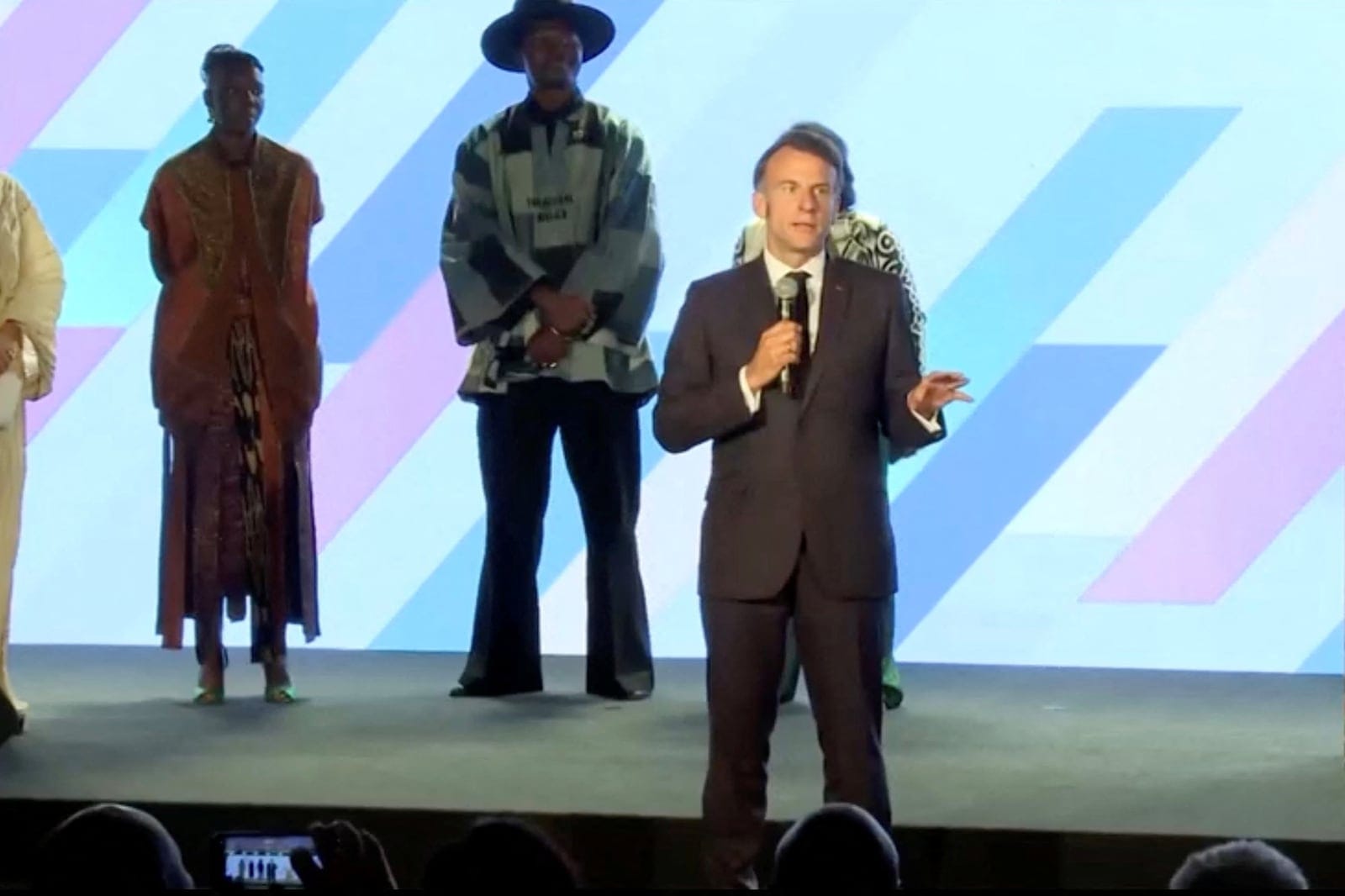

Macron seeks to rebuild France’s profile in Africa

France’s President Emmanuel Macron this week sought to enhance his country’s engagement with Africa, announcing some €23 billion in investment commitments at a summit in Kenya’s capital Nairobi, Business Day reports. The summit, the first France has held in an English-speaking African country in more than five decades, follows political ruptures and military withdrawals from Mali, Burkina Faso, Niger and Chad.

Shipping company CMA CGM signed the headline deal, a €700 million agreement to expand capacity at Kenya’s Port of Mombasa. Proparco, the development finance arm of the French government, closed over €500 million in deals in a single day, including a €300 million facility with Ecobank for agricultural lending across 33 countries and €300 million with AXIAN Group for telecom and renewable energy.

In total, €14 billion will come from French investors, with African partners contributing €9 billion.

African leaders used the second day to push for structural reforms to credit risk assessments, arguing they face borrowing costs twice as high as advanced economies. Macron backed a guarantee mechanism to de-risk investment on the continent and pledged to lobby for the proposal at the G7 summit in Evian next month.

Asia

MSCI rebalance drops Indonesia stocks

Index provider MSCI dealt a blow to investors in Indonesia on Wednesday with a decision to remove six Indonesian companies from its country index, Reuters reports.

Although investors anticipated the decision, the country’s benchmark JKSE index fell 2% to the lowest level in more than a year. Securities analysts said the expulsions could trigger up to $1.7 billion in capital outflows as foreign funds that track Indonesia rebalance their holdings, Nikkei reports.

MSCI flagged transparency concerns over Indonesian stocks in January, stoking fears that the index provider could downgrade the country to frontier-market status. The firm is currently conducting a review of Indonesia’s market that is set to conclude in June.

Pakistan inks energy deal with Iran

Pakistan has worked out a deal with Iran to ship liquified natural gas through the Strait of Hormuz, Reuters reports. Two tankers filled with LNG from Qatar are now on their way to Pakistan.

Pakistan imports 40% of its energy, according to the World Bank, with much of that coming from the Gulf. Many tankers remain stuck at port despite a ceasefire in the US/Israeli war on Iran, and Pakistan has raised fuel prices by more than 50% since the beginning of the conflict in February, Arab News reports. Iraq made a similar oil shipping arrangement with Iran this week, according to Reuters.

Pakistan is playing a key mediation role in the war, but it came under fire this week after a CBS News report on Tuesday said that it had allowed Iran to park jets on its airfields.

Vietnam’s South China Sea island-building expands sharply

Vietnam has added more than 500 acres of land in the past year to its islands in the Spratly archipelago, a report by the Washington-based Center for Strategic and International Studies found.

Vietnam has now built 2,771 acres of artificial islands in the area, according to the report. But China, which also claims the Spratleys, has built nearly double that area. The report said that China has constructed 5,460 acres of artificial land, including Antelope Reef, which it said is likely the largest island in the South China Sea.

Despite the island-building competition, Vietnam has sought to maintain good relations with China. Last month, Vietnamese leader To Lam visited Beijing, where the two countries signed 32 cooperation agreements in areas including rail infrastructure and digital technology.

Middle East

Saudi Arabia strikes delicate balancing act with Iran

Saudi Arabia launched covert attacks against Iran in late March, described as tit-for-tat retaliation to establish deterrence, Reuters reports. Despite the exchange, Saudi Arabia and Iran have maintained bilateral communication lines, and coordinated de-escalation to prevent the conflict from spiraling further, with Riyadh signaling that it was only acting in self-defense and not joining the broader US-Israeli war on Iran.

The decision to launch strikes came in late March, in response to Iranian drone and missile attacks against Saudi energy infrastructure. Riyadh had previously warned Tehran of its red lines, which were later crossed.

Since the exchange, Saudi Arabia has supported mediation efforts by Pakistan and went as far as closing its airspace during last week’s short-lived US effort to pry open the Strait of Hormuz, which Riyadh saw as an aggressive, escalatory step counterproductive to negotiations.

- Saudi oil giant Aramco’s profit soars on higher prices (Zawya)

- Aramco aims to raise $10bn from property portfolio (Bloomberg)

Saudi Arabia is considering pursuing a non-aggression pact with Iran based on the 1975 Helsinki Accords, part of a broader foreign policy rethink as it adjusts to the aftermath of the US-Israel-Iran War, the FT reports. Some EU countries are reportedly supportive of the idea and urging other states in the Middle East to join, although the UAE, whose rift with Saudi Arabia is widening, is said to be opposed to the strategy, and is taking a more aggressive anti-Iran stance.

Syria sees progress in oil and gas sector

Syria this week finalized the site for its first deep-water oil and gas exploration project with US giant Chevron and Qatar’s UCC Holding, Reuters reports. The selection is a major milestone in the partnership created in February, and paves the way for contract finalization and commencement of technical operations this summer.

- EU agrees to restore full trade ties with Syria (Al Jazeera)

- UN food agency halves Syria food aid over funding shortages (Reuters)

Other major energy companies are expressing interest in Syria’s oil & gas potential. TotalEnergies, ConocoPhillips, and QatarEnergy this week signed a deal with the Syrian Petroleum Company to launch a technical review of another offshore block.

The UAE is also considering ramping up investment into Syria. A group of Emirati businesses this week visited Damascus to discuss a potential $18 billion in real estate and tourism projects.

Europe

Hungary’s new government moves quickly to fulfill promises

Hungarian Prime Minister Peter Magyar’s government, which took office this week, has doubled down on pledges to move the country toward euro adoption and reduce the deficit from an anticipated 7% by the end of this year to 3% in 2030 through policies aimed at increasing growth and eliminating corruption, Reuters reports.

Since being sworn in, Magyar has extended veto power to four ministers as a check on his own power and condemned a drone attack by Russia on Ukraine, sharp departures from former prime minister Viktor Orbán’s autocratic behavior and close relationship with Moscow.

Widening deficits in Eastern Europe spark investor concern

Investors and sovereign credit rating firms are growing increasingly concerned about the interplay of widening deficits, policy changes and economic growth rates in the Czech Republic, Poland and Romania as the investment environment becomes more complicated, Reuters reports.

Poland continues to increase spending on defense, which the government has doubled since Russia’s full-scale invasion of Ukraine in 2022. Poland’s deficit has increased steadily from 3.4% to 7.3% in 2025, but steady economic growth has eased investors’ concerns about the country, according to Dutch bank ING. But high energy prices may drive a reduction in consumption and could challenge Poland’s economic balancing act.

Romania is also being monitored closely as a new government will need to grapple with unpopular tax hikes and other reforms enacted by the outgoing government to avoid a credit downgrade. The political uncertainty—and potential future challenges to fiscal consolidation measures—make it more likely Romania’s credit rating will be downgraded, research firm Oxford Analytica forecasts.

Latin America

Fujimori and Sanchez confirmed for Peru election runoff

Conservative Keiko Fujimori and leftist Roberto Sanchez will face off in Peru’s June 7 presidential runoff after Sanchez narrowly beat right-wing rival Rafael Lopez Aliaga with 99% of ballots counted, Reuters reports.

Sanchez, a close ally of jailed former president Pedro Castillo, has pledged to rewrite the constitution, phase out open-pit mining, review tax agreements with major operators, and redirect international reserves toward social spending. Hours before Sanchez’s spot in the runoff was confirmed, Peru’s public prosecutor charged him with campaign finance violations, France24 reports.

Concerns are rising that a Sanchez victory could put off mining companies from investing in Peru, Mining.com reports. Peru is the world’s third-largest copper producer, with mining accounting for approximately 60% of exports and anchoring operations for Glencore, Anglo American, Freeport McMoRan, and MMG.

Colombia’s debt surges to 55% of GDP

Colombia’s total external debt rose by approximately $30 billion over the past year as the government of President Gustavo Petro relied increasingly on external financing to cover a widening fiscal deficit, ColombiaOne reports.

Public external debt now exceeds $157 billion, with the increase driven by international bond issuances, multilateral loans, and higher long-term obligations. Tax revenues have underperformed expectations amid an economic slowdown, and multiple Petro administration tax reform initiatives have been blocked by Congress or struck down by the courts.

Credit rating firms have warned that rising debt-servicing costs and potential peso depreciation could further strain public finances. The debt-to-GDP ratio showed a slight improvement in early 2026 as the peso appreciated in some months, but the absolute volume of obligations continues to climb.

Argentina upgrades opens debt-market window

Fitch Ratings this week upgraded Argentina’s sovereign credit score to B- from CCC+, fueling speculation that the country could tap international debt markets for the first time since its 2020 restructuring, Buenos Aires Times reports. Investors describe the window as “real but narrow,” with 2027 effectively closed by the political calendar when President Javier Milei is expected to seek a second term.

The country’s existing 2035 bonds rallied on the news, although economy minister Luis Caputo has indicated the government is in no rush to tap markets, noting it can still access local financing at roughly 6% against external bond yields near 9.5%.

The positive market signal comes despite President Javier Milei’s approval rating falling to 35.5% amid corruption scandals in his cabinet and mass protests over university budget cuts.

What We’re Reading

Senegal’s president ‘personally handling IMF debt talks’ (Reuters)

Ghana eyes buying sanctions-hit Lukoil’s stake in oil block (Bloomberg)

Zambia’s copper output down 4% in the first quarter (CNBC Africa)

DRC rebels pull back from key positions amid US pressure (Reuters)

Republic of Congo requests new IMF program to tackle debt (Bloomberg)

South Africa’s Ramaphosa turns to courts to stall impeachment (Semafor)

Morocco launches national desalination industry (North Africa Post)

Philippines VP impeached (Rappler)

Thailand ex-PM Thaksin released from prison (Bangkok Post)

Kyrgyzstan charges ex security chief with plot to seize power (Reuters)

Turkey scraps inflation target as economic strains deepen (FT)

Lebanon’s central bank tightens lira supplies as financial pressures mount (L’Orient Today)

Kuwait approves Saudi Arabia rail link route (Zawya)

Latvian government collapses amid dispute over breaches by Ukrainian drones (WaPo)

Poland stands by digital services tax plan, rebuffing US threats (Bloomberg)

Bidding for comeback, Kosovo’s opposition LDK bets on ex-president Osmani (Balkan Insight)

Former chief of staff of Ukraine’s Zelenskyy targeted in major corruption probe (FT)

Bulgaria ends state-funded protection for ex-PM and sanctioned oligarch (Balkan Insight)

CIA chief visits Cuba as energy crisis worsens (BBC)

Paraguay’s economy reports almost 5% growth in first quarter (Asuncion Times)

US deportations to El Salvador double as Bukele aligns himself with Trump agenda (AP)

Venezuela launches effort to ease $170bn debt load (WSJ)

We are committed to providing FMN readers with a free weekly digest of politically unbiased, succinct and clear news and information from frontier and small emerging markets.

Please consider becoming a paid supporter to help cover some of our costs and support our continued development of sharp markets-focused coverage and new informational products. Paid subscribers will also gain exclusive access to our EM/FM reports that aggregate insights from dozens of major banks, international institutions and consultancies.

Read next